While the industry was busy debating prediction markets and crypto convergence, Brussels quietly dropped a regulatory bomb. No fanfare. No emergency sessions. Just a political agreement that changes the business of running a retail broker from A to Z. Meet the Retail Investment Strategy. Agreed in December 2025. And somehow still missing from most brokers’ radar.

Here is the short version. The EU decided that retail investors deserve better. Fairer fees. Honest advertising. Clearer products. And somebody to b lame when things go wrong. Spoiler: that somebody is you.

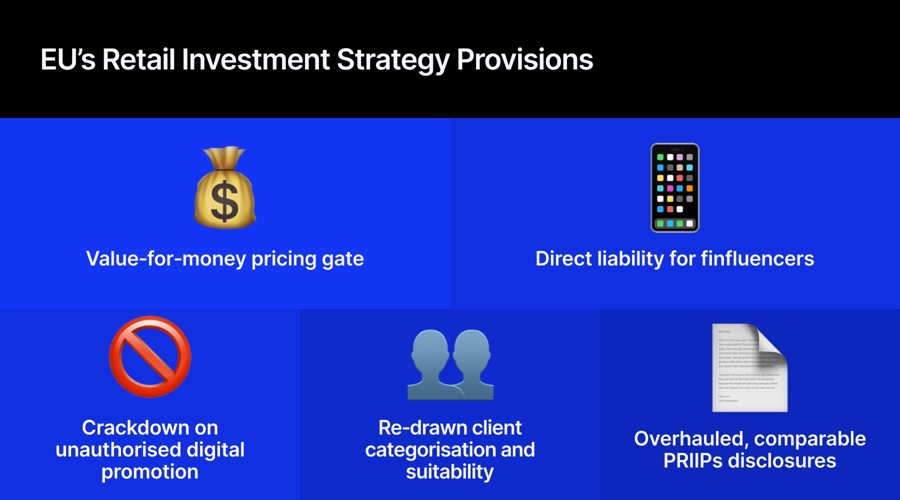

Your Pricing Just Got a Referee

For a decade, the compliance conversation in this industry has been about disclosure. Show the client what they are paying. Put it in the KID. Send the cost statement. Job done. Go home.

That era is over.

The centrepiece of the RIS is three words: value for money. Under the new rules, manufacturers and distributors must identify every cost an investor bears and prove those costs are justified and proportionate. Products will be tested against peer-group benchmarks of comparable instruments. If your product charges materially more than the peer group with no defensible reason, it should not be approved for sale to retail investors.

MiCA Countdown: 7 Days to GoWhat is changing on 1 July 2026?On 1 July 2026, a significant milestone will be reached in the implementation of the EU’s Markets in Crypto-Assets Regulation (MiCA).For many crypto-asset service providers, this marks the end of the transitional… pic.twitter.com/vHobV2D9EQ

— CryptoUK 🇬🇧 (@CryptoUKAssoc) June 24, 2026

Not just disclosed. Not just flagged. Not approved for sale.

For CFD brokers and social trading platforms, this lands directly on spread pricing, overnight financing rates, and conversion fees. These have historically been competitive weapons.

Continue reading: NAGA Wins EU Crypto License Days Before MiCA Deadline

Ways to win clients at the front end while recovering margin through the product. The RIS puts a benchmark microscope on that entire model. This is the clause that rewrites your pricing strategy, product governance, and distribution economics simultaneously. And it is the one that most operators have not connected to their P&L yet.

Your Finfluencer Just Became Your Liability

The second major provision is the one that will quietly reshape acquisition channels everywhere. The EU’s approach to finfluencers is not to license them. It is far smarter and far more uncomfortable for brokers. It makes you responsible for them.

Where a broker uses a social media personality to promote products, the firm must hold a written agreement with that person, maintain their contact details on file, and exercise documented control over what they post. Marketing must be fair, clear, and not misleading across all digital channels. Everything gets archived for the life of the client relationship.

The Influencer Posts. The Broker Answers

Every paid promotion, every commission-based content creator, every brand ambassador arrangement now sits inside your compliance perimeter. Content review, contractual framework, record-keeping.

All of it becomes a supervisory expectation, not a nice-to-have. A new MiFID Article 5a also targets unauthorized activity through digital channels, and a new ESMA database will publicly name entities caught operating without authorization. The era of loosely governed digital promotion in retail finance is closing fast.

Three More Changes Most Brokers Are Sleeping On

Investor categorization gets reformed. Clients can now opt for professional status more easily. The portfolio threshold drops, and a new education criterion is added. For CFD operators, a wave of reclassification requests is a plausible near-term outcome. Professional status changes the leverage and protection picture significantly.

Suitability requirements are simplified for non-complex, cost-efficient products. Lower friction for retail investors entering markets. That is the whole macro point of the EU’s Savings and Investments Union agenda.

You may also like: “New EU Rules May Attract More Serious Asset Managers to Cyprus,” Says CySEC Chair

PRIIPs Key Information Documents get rebuilt with a clean product-at-a-glance section covering costs, risk, and recommended holding period. KIDs also become machine-readable, enabling direct product comparison. Benchmark-ready disclosure is no longer optional.

The Clock Is Ticking. But You Still Have Time

The Official Journal publication is expected by mid-2026. From that date, firms have 30 months to comply. That puts the hard deadline at the end of 2028.

Thirty months sounds generous. It is not. Rebuilding pricing governance, formalising influencer frameworks, restructuring product disclosure, and stress-testing your cost model against a benchmark that does not exist yet takes longer than most compliance teams expect.

Άρθρο του Δρ. Θεοχαρίδη με θέμα Σταθερή ανάπτυξη της κεφαλαιαγοράς υπό το βλέμμα της ΕΚΚ στον «ΦΙΛΕΛΕΥΘΕΡΟ»Article by Dr. Theocharides titled “Steady development of the capital market under the supervision of CySEC” in “Phileleftheros”. (in Greek)https://t.co/TRoNtd2Cik

— CySEC – Cyprus Securities and Exchange Commission (@CySEC_official) January 13, 2026

The firms that treat this as a 2028 problem will spend 2027 in emergency mode. The firms that treat it as a 2026 strategic priority will have rebuilt their model before the regulator even shows up.

CySEC Chairman George Theocharides has said it consistently. The rules come from Europe. Not from national regulators moving independently. From Europe. He was right. The rule is now agreed. And the clock started in December.

The question is not whether this changes your business. It already has. The question is whether you find out now or in 2027 when the pressure is real, and the runway is gone.

This article was written by Badea Alexandru Gabriel at www.financemagnates.com.Retail FXRead More

You might also be interested in reading Bitcoin Apparent Demand Remains Weak — What This Says About Price Recovery.