Polymarket has officially crossed $65B in cumulative volume. But while the world watches the charts, I wanted to see who is actually building the tools underneath that volume.

As part of a new report, I dug into 114 different projects, from automated market makers to specialized media outlets, to map out the “Missing Middle” of this ecosystem.

Here is what the data actually says about the state of prediction market builders:

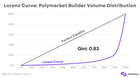

The 0.83 Gini CoefficientWe often talk about wealth inequality in crypto, but the builder inequality on Polymarket is staggering. It’s more concentrated than the S&P 500.

The “Elite 6”: Just 6 builders control 81% of all lifetime third-party volume ($1.31B). The Outlier: An entity called Betmoar has processed $817M. To put that in perspective, that is more than the rest of the top 50 projects combined. The Median Reality: Most builders are struggling. The median project processed just $20,000 in volume in Q1 2026. The Native Funding GapPolymarket is processing roughly $8B–$10B in monthly volume, yet the venture capital reaching native builders is a rounding error.

While giants like Jupiter and Based have raised millions, they aren’t “Polymarket-native.” For projects built specifically for this ecosystem, total native funding sits at just ~$20M. The infrastructure is scaling at lightspeed, but the dedicated builder layer is dangerously under-capitalized. The “Ghost Founder” ParadoxThis was the most surprising find: Traction and visibility are completely decoupled. In most of DeFi, “shilling” comes before volume. Here, it’s the opposite.

Anonymous Growth: Only 25 of the 114 builders we tracked have an identifiable founder or public presence. Media Silence: Despite $26B in quarterly volume, only 18 projects have ever received third-party media coverage. The Invisible King: Betmoar (the volume leader) has zero public brand, zero press, and no identifiable face. The “Golden Quadrant” is EmptyWhen I mapped these projects on a matrix of Visibility vs. Traction, the top-right quadrant (High Traction/High Visibility) was a total void.

Most projects are “Ghosts”, they have the volume but no brand. This is a massive risk. In a platform-dependent ecosystem, volume is a trailing indicator. Brand equity is the only leading indicator that survives an API change or a competitor launch.

The Conclusion: The next phase of prediction markets won’t be won by the person with the best algorithm; it will be won by the first builders who successfully move from being “anonymous tools” to “identifiable brands.”

I’ve put the full breakdown, including the ecosystem map and methodology, in the report here: https://www.chainstory.co/the-invisible-ecosystem-who-actually-builds-on-polymarket/

submitted by /u/EmbarrassedStudent10 [link] [comments]

r/CryptoCurrencyRead More

You might also be interested in reading Bitcoin price over $20K creates FOMO with 620K new BTC wallets.